Air, Freight News

Early Lunar New Year masks falling China e-commerce exports

[ February 6, 2026 // Chris Lewis ]

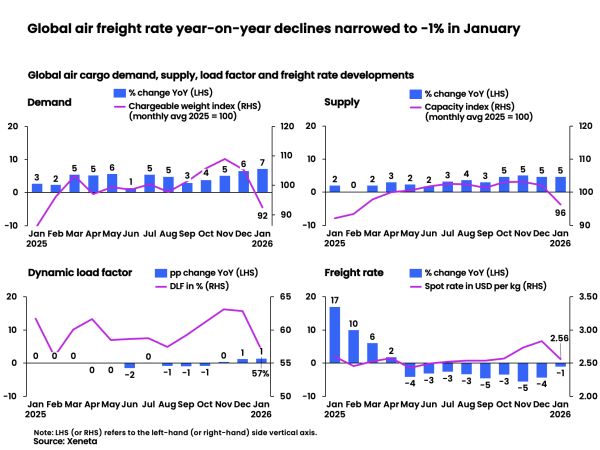

An earlier Lunar New Year flattered global air cargo demand in January as the year commenced with unexpected vigour with a +7% year-on-year boost in demand and an easing of recent freight rate declines, says industry analysts Xeneta. However, any early market optimism for 2026 was dampened by the first year-on-year fall in e-commerce exports from China since January 2022.

The growth in global chargeable weight in the opening month of 2026 was the strongest increase since January 2025, and ahead of the +5% year-on-year growth in capacity supply. With volumes rising faster than capacity, the global dynamic load factor edged up one percentage point to 57%. Dynamic load factor is Xeneta’s measurement of capacity utilisation based on volume and weight of cargo flown alongside available capacity.

Recent pricing declines also recovered with global air cargo spot rates down just -1% year-on-year to US$2.56 per kg in January.

However, Niall van de Wouw, Xeneta’s chief airfreight officer, said the relative upbeat nature of the air cargo market in January needs to be’ tempered with a dose of reality’.

“Asia is such a big exporter of airfreight, it is difficult to draw any conclusions on what the market is signalling in January because of the Lunar New Year and the fluctuations it causes,” he said. “In 2025, the festivities began on 28 January but this year, they begin on 15 February, so much of January’s strength in air cargo volumes is likely calendar-related rather than a clear indicator of improvements in underlying demand.”

Similarly, he said the picture for global air cargo spot rates in January may be a truer reflection of world economic events than demand for capacity. Air freight rates are typically quoted in local currencies, so a weaker dollar can make a world average – converted back into dollars – look firmer than it truly is.

More decline in e-commerce volumes ex-China

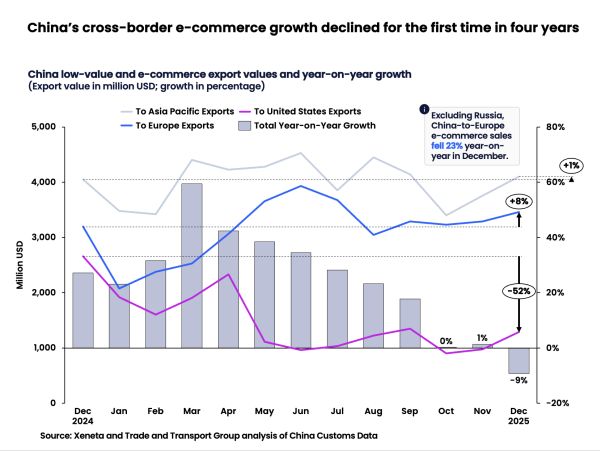

While the outlook for demand and air cargo rates is unlikely to become clearer until the end of the first quarter, one undeniable fact certain to influence air freight volumes is the drop-off in e-commerce volumes ex China and Hong Kong.

Latest China Customs data for December shows low-value and e-commerce exports falling -9% year-on-year, the first decline since January 2022 following two months of flat growth. For an air cargo market that has been turbocharged by cross-border e-commerce since late 2023 – and which relies on e-commerce for some 20-25% of its total annual volumes globally – this is a trend airline and freight forwarders will be closely monitoring.

With the US de minimis ban now firmly in place, China-to-US e-commerce exports extended their steep decline, down more than -50% for a third consecutive month in December. For full year 2025, e-commerce exports fell -28% versus the prior year.

The move by China’s big e-commerce platforms to grow their share of the European market, to offset higher costs impacting volumes into the US, has provided more positive news on this corridor in recent months, but this, too, is now looking exposed.

The growth of China-to-Europe e-commerce volumes slowed to roughly +8% in December compared to a growth rate of +54% over the first 11 months of 2025. And, when excluding Russia, e-commerce sales from China to the rest of Europe declined a considerable -23% year-on-year.

Van de Wouw said: “In October, we said air cargo’s e-commerce growth engine was showing signs of slowing down, but that this could be just a blip. We saw this again in November, and we said if it happened for a third consecutive month in December, this would signal a trend. This is now the situation.

“If it remains flat or declines further, it will certainly affect many organisation’s growth plans, including those with commitments to freighter conversions that will be relying on the high level of e-commerce demand we have seen in recent years.”

Regulation is undoubtedly a factor adding friction to e-commerce trade. US de minimis bans, the EU’s proposed processing fee, and new rules in Japan and Thailand all threaten to dull one of air freight’s most reliable sources of demand.

Red Sea return may dampen airfreight

Developments in ocean container shipping remain a key wildcard for air freight growth, with the Red Sea/Suez situation requiring close attention. Since late last year, major carriers such as CMA CGM – and more recently Maersk – have been testing Suez Canal routings on selected sailings.

The latest signal from the Gemini partners (Maersk and Hapag-Lloyd) is that the India–Mediterranean loop will resume Suez Canal transits this month, enabled by naval protection and the “highest possible security precautions” to protect crew, vessel and cargo safety. This is a more concrete step than “test” voyages and is being seen as a tentative move toward broader normalization – albeit still conditional on security.

But reality can still intervene quickly and any disruption is likely to lead some ocean shippers back into the air freight business, at least in the short-term. CMA CGM has shown how fragile the situation remains, having previously resumed Suez Canal transits on some backhaul voyages before reverting two services to the Cape of Good Hope due to a “complex and uncertain international environment”.

Even if the Red Sea were to improve further, a rapid modal shift from air back to ocean still looks unlikely in Q1 2026. Many container vessels are still being diverted around Cape of Good Hope routings, transit times are still lengthy (often well beyond six weeks depending on rotation and congestion), and network-wide schedule/capacity reallocation back to the Suez Canal is operationally difficult to execute within a single quarter.

In the near-term, this uncertainty may help to ensure the demand gap in air freight volumes caused by fewer e-commerce shipments doesn’t widen further.

Spot rate decline

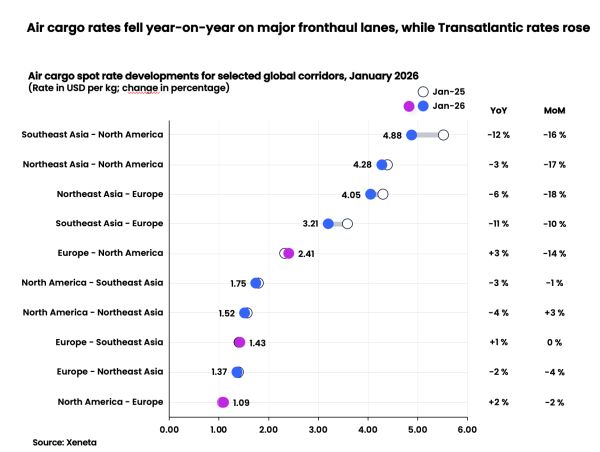

At the corridor level, most air cargo spot rates continued to decline year-on-year in January, broadly in line with the global market trend.

The steepest falls were on Southeast Asia to North America and Southeast Asia to Europe, where spot rates dropped by more than -10% year-on-year as capacity continued to expand. Month-on-month, both corridors also fell between 10 and 16%, reflecting their exposure to seasonal demand weakness.

Northeast Asia to Europe recorded the third-largest year-on-year decline, down -6% in January. This suggests capacity growth is outpacing demand, likely influenced in part by softer cross-border e-commerce growth. By contrast, Northeast Asia to North America saw only a modest -3% year-on-year decline, largely driven by the agile removal of freighter capacity.

As with outbound Southeast Asia, both outbound Northeast Asia corridors also posted close to a -20% month-on-month decline as the market temporarily moved into the off-peak period. Spot rates are expected to show an uplift ahead of the Lunar New Year in mid-February, although there are currently few signs of a pre-Lunar New Year cargo rush.

Transatlantic tariffs

On the Transatlantic westbound corridor, spot rates unexpectedly rose +3% year-on-year, despite a -4% year-on-year decline in chargeable weight. This divergence may partly reflect the recent US tariff threat – an additional +10% on imports from eight European countries – before it was reversed on 21 January. This demonstrates both the responsiveness and nervousness of shippers trying to protect their product margins.

The withdrawal of the tariff threat by the US administration certainly appears to have prompted a temporary demand bump: in the week ending 25 January, volumes rose +16% week-on-week, a period that typically sees only low single-digit growth. However, a weaker dollar – making EUR-quoted air freight more expensive – may be a larger factor behind the rate strength.

Tags: Xeneta